Authored by Lance Roberts via RealInvestment Advice.com,

As I noted in yesterday’s missive, Yellen’s recent testimony on Capitol Hill sent robots frantically chasing asset prices on Thursday even before testimony began. The catalyst was the release of prepared testimony which included this one single sentence:

“Because the neutral rate is currently quite low by historical standards, the federal funds rate would not have to rise all that much further to get to a neutral policy stance.”

And on that statement, doves flew and algorithms kicked into to add risk exposure to portfolios. Why? Because she just said that rates will remain low forever. As my partner, Michael Lebowitz, noted yesterday:

“Per Janet Yellen’s comment, the ‘neutral policy stance’ is another way of saying that the Fed funds rate is appropriate or near appropriate given current and expected future economic conditions. Said differently, Janet Yellen is admitting what we’ve been saying for years – the economy has been stagnant, is stagnating and will continue to stagnate.

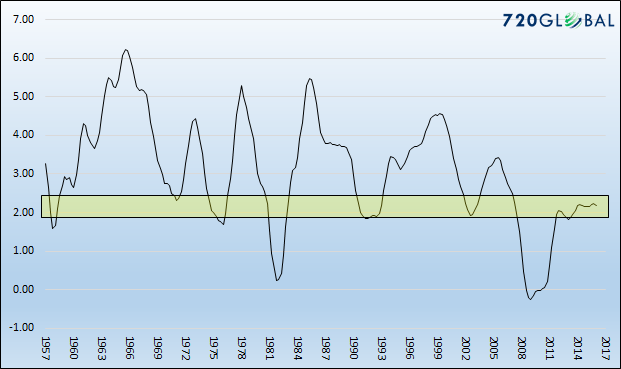

If we assume that Yellen is referring to a range of 1.25-1.75% as an appropriate Fed Funds rate, based on statistical analysis of data since 1955, we forecast that real GDP growth rate is likely to average somewhere between 2.00-2.50% for the foreseeable future. For perspective, the graph below plots the range of expected GDP growth vs historical secular (3-year average) GDP growth. In years past, such a slow rate of growth (highlighted in yellow) was considered nearly recessionary.”

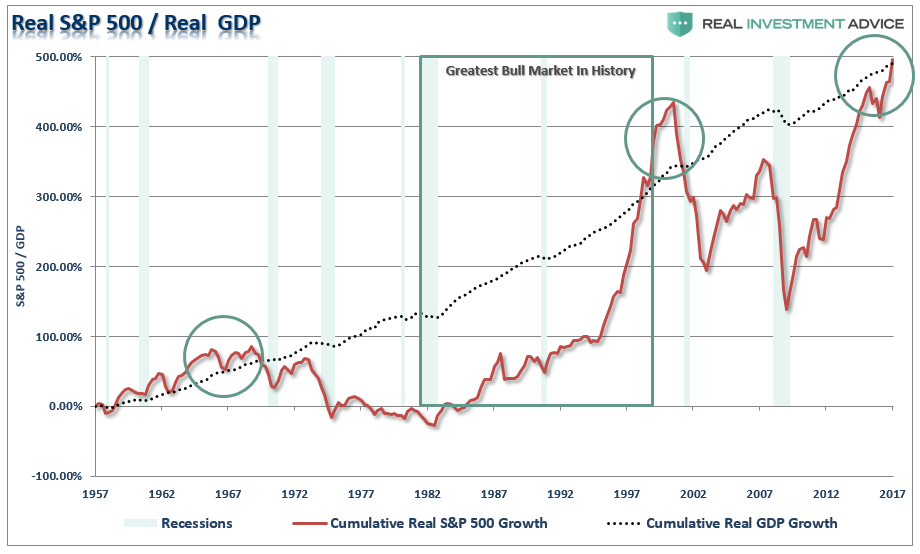

The problem, of course, is that a 2% economic growth rate is not conducive to a strongly expanding economic environment and does not support current market valuations. The first chart below compares the cumulative growth rate of the real S&P 500 as compared to GDP. The great “bull markets of the 50’s and 60’s, the 80’s, and now the 10’s have all previously ended when the growth of the S&P 500 exceeded the growth of the economy.

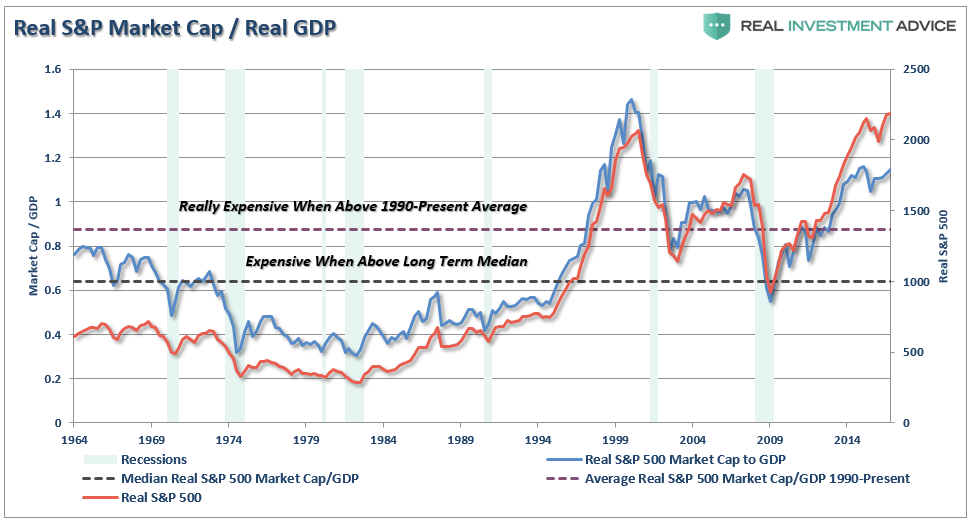

The next chart compares the inflation adjusted market capitalization rate of the S&P 500 to GDP. As noted on Tuesday, valuations have everything to do with forward returns on investments over the long-term.

The problem for the Fed remains the rising risk of a monetary policy error against a backdrop of an over valued, over leveraged and overly bullish financial market. Historically such combinations have tended not to turn out well.

While markets may well continue to remain bullish in the short-term, the longer-term outcomes remain heavily weighted against investors currently. Of course, the “chase for return” is always the most prevalent when markets remain illogical longer than investors can remain rational.

In the meantime, this is what I am reading.

Politics/Fed/Economy

- Trump’s Very Own “Big Fat Ugly Bubble” by David Stockman via Daily Reckoning

- Will Low Inflation Delay Rate Hikes by James Picerno via Capital Spectator

- Fed’s Could Use Some Target Practice by Caroline Baum via MarketWatch

- Jim Chanos: Economy Worse Than You Think by INET Economics

- Fed Has Put Markets In Survival Mode by Dean Cumutt via Bloomberg

- 4-Signs The Economy Is Stalling by Stephen McBride via Mauldin Economics

- The False Premise Of GOP Tax Cuts by Editorial via New York Times

- Monetary Policy Continues To Fail Society by Third Wave Finance

- “MAGAnomics” On Its Way by Bob Bryan via Business Insider

- New Senate Health Care Bill Looks Like ACA by Tyler Durden via ZeroHedge

- Beware New Abnormal Monetary Policy by Nouriel Roubini via Project Syndicate

- Social Security Budget Nightmare Must Be Resolved by Blahous & Reischauer via CNBC

Markets

- Will Corporate Bonds Cross Over by Danielle DiMartino-Booth via Money Strong

- Stock Market Tsunami Warning Rings by Wolf Richter via Wolf Street

- A Skeptics View Of Popular Stocks by Leslie Norton via Barron’s

- History & Gravity Aren’t On The Side Of Stocks by Sue Chang via MarketWatch

- Stock Picking Dying Due To Dearth Of Stocks by Jason Zweig via WSJ

- Perfect Market Indicator Says Sell Now by Mark Kolakowski via Investopedia

- Beware Of The Stock Market by Joe Ciolli via BI

- Sometimes, The Best Advice Is “Do Nothing” by Simon Constable via US News

- BlackRock: Forget Low Volatility by Joe Ciolli via BI

- Bull Market Ain’t Dead Yet by Michael Kahn via Barron’s

- Summer Investing Reading List by Neil Dwane via MarketWatch

- Recession Could Be Coming by Comstock Partners

- Big Change In Sentiment Coming by Peter Atwater via Hedgeye

- Funds To Consider In A Bear Market by John Coumarianos vis WSJ

- Stock Market 66% Over Valued by Thomas Kee via MarketWatch

Research / Interesting Reads

- “Carmageddon” Hits Houston by Wolf Richter via Wolf Street

- The Fast Track To “Carmageddon” by David Stockman via Daily Reckoning

- Millennials Not Helping Housing Problem by Mark Hanson via MHanson.com

- A Chat With Peter Bernstein by Jason Zweig via Intelligent Investor

- The Development Of The “Perfect Storm” by Robert Huebscher via Advisor Perspectives

- 5 Mistakes That Can Ruin Your Future by Christy Bieber via The Motley Fool

- Habits To Bring Out The Best In Others by Stephanie Vozza via Fast Company

- Our Financial Buffers Are Thinning by Charles Hugh Smith via Of Two Minds

- The Art Of Getting S**T Done by What I Learnt On Wall Street

- Working Past 70, Americans Can’t Retire by Ben Steverman via Bloomberg

- Japan Hits Unlimited Money Printing Panic Button by Jared Dillian via Maulding Economics

- Yellen Warns Congress Debt Trajectory Unsustainable by Tyler Durden via ZeroHedge

- Stall Speed by John Hussman via Hussman Funds

- A Lowly Bounce In Tech Stocks by Dana Lyons via Tumblr

- Rising Rates A Problem For Risk Assets by Jesse Felder via The Felder Report

“Most investors want to do today what they should have done yesterday.” – Larry Summers